Imagine yourself walking into a dark alley, in the middle of some ghetto neighborhood, and halfway through, a masked thug suddenly appears, pulls out a sharp knife and exclaims, “Your Money or Your Life!” Unless your first name is Chuck and your last name is Norris, chances are, you would surrender your wallet before running in the opposite direction.

For the same reason, you wouldn’t run into a burning house to save your valuable possessions. You wouldn’t dive into shark-infested waters to retrieve a $100 bill either. Otherwise, you really have to question your priorities or judgment.

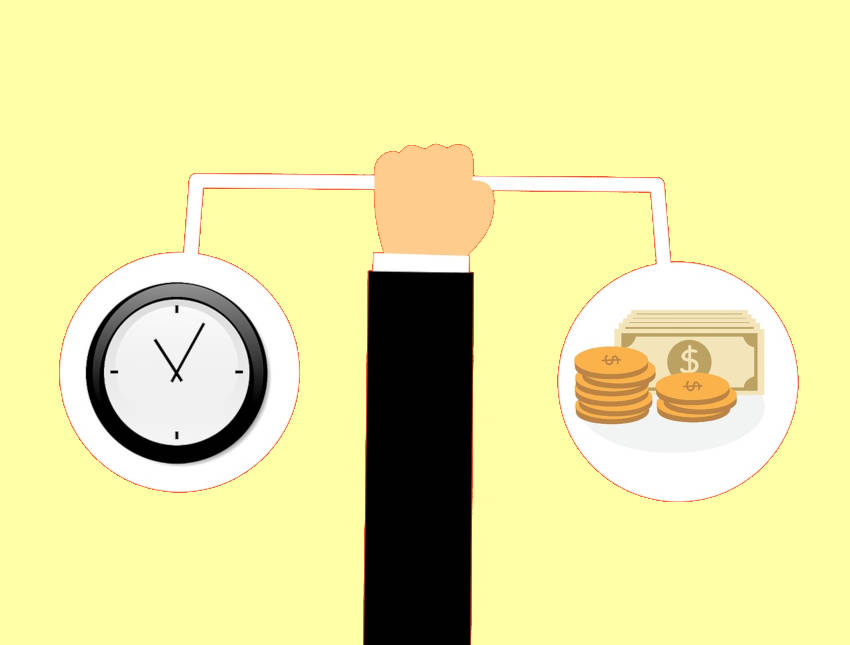

Let’s face it. No matter how cash-starved you are; your life is more precious to you than your money. This is true for everyone. But what many people don’t realize, they are already routinely trading segments of their precious lives in exchange for money. The money they use to buy stuff and more stuff that won’t necessarily contribute to their happiness.

I believe that’s the main issue that authors Vicki Robins and the late Joe Dominguez tried to address when they wrote the New York Times bestseller, “Your Money or Your Life.”

A book that transforms your relationship with money

Originally published in 1992, the book’s premise is that you exchange your valuable time for money. And when you start thinking about how many hours of your life it took to save up the money to buy something, you really start thinking twice about your purchases.

So let’s say you work eight hours a day, and after taxes, make $10 an hour– you’re basically earning $80 a day. You then stumbled upon this really nice pair of shoes on Amazon that costs about $80. That moment when you click Buy, you essentially spent an entire day of your life working for those shoes. And when you start thinking about large purchases, like that 65″ high-definition TV, and you’d start asking yourself, “How much of my life did I trade for this? Is it really worth it?”

Money is something we choose to trade our “life energy” for and this realization transforms how we interact with money. The things that you and I buy, they better be worth it. More will no longer feel like better.

9 steps to achieving Financial Independence

The book offers nine simple, “common sense” practices that you can apply to transform your relationship with money, and consequently, achieve Financial Independence.

Step 1: Making peace with the past

This step asks you to tally your lifetime earnings. If you don’t have that information, make an estimate based on your past employment instead. Create a balance sheet. Subtract all your debt from your assets to determine your net worth. You might get disappointed, but that’s okay, the fact that you’re reading this post is a step in the right direction.

Step 2: Being in the present — tracking your life energy

The first part is to know how much are you are trading your life energy for. You’ll learn that your real hourly wage is much lower than you think it is if you subtract the following:

- Your federal, state, and local taxes

- Work-related expenses such as commuting costs

- Stress-reducing activities

You can use the Life Energy Calculator directly from the book’s website if you want.

The second part is to keep track of every penny that comes and goes out of your life. This way, you become conscious of the amount of money that actually comes and goes in your life.

Step 3: Where is it all going?

Track your income and tally spending categories, and convert your expenses into “hours of life energy” spent. For example, Eating out: 30 hours, etc. I wrote about creating a yearly household report before, but this step requires you to do a detailed breakdown on a monthly basis.

Step 4: Three questions that will transform your life

For each of the categories above, ask yourself:

- Did I receive fulfillment in proportion to the hours of life energy spent?

- Is this expenditure in alignment with my goals and life purpose?

- How might this expenditure change if I didn’t have to work for a living? (more, less, same)

Step 5: Making life energy visible

Create a chart to visualize the data you’ve gathered in previous steps, plotting them on a graph that shows a clear picture of your financial situation. You can create an Excel or Google spreadsheet online or post it on the fridge if you’re not tech-savvy. Make a habit of updating this chart over time. This way, you will learn to spend more consciously.

Step 6: Valuing your life energy — minimizing spending

Your life is limited, don’t waste it living someone else’s life. Everything you value has to fit inside that life– falling in love, getting married, time spent with kids, etc. Not to mention that you spend a third of that life sleeping!

We should learn how to spend our money efficiently on things that we get true fulfillment from.

Step 7: Valuing your life energy — maximizing income

Think of your job as just a means to end. It doesn’t really matter whether you love your paid employment or hate it. The real purpose of paid employment is getting paid! Remember, this step is temporary. There’s light at the end of the tunnel (next step).

Step 8: Capital and the Crossover Point

“Capital is money that makes more money. It keeps working for you and produces income as surely as your job produces income. When you put capital in a bank or other interest-bearing instrument it is an investment.”

The Crossover Point is when the passive income from your investment equals your living expenses. It now becomes clear why the book wants you to minimize your spending and maximize your income (Steps 6 and 7)– that’s the fastest way you can achieve Financial Independence!

Related: Suze Orman Could be Right, This Calculator Can Tell You Why

Step 9: Managing your finances

The final step to financial independence is, to quote the author, “Become knowledgeable and sophisticated about long-term income-producing investments and manage your finances for a consistent income sufficient for your needs over the long term.”

Here’s my take

Your Money or Your Life is a very inspiring and powerful resource for anyone that is seriously interested in becoming Financially Independent. In fact, it has become the unofficial “Bible” of the Financial Independent Retire Early (FIRE) movement. There’s a reason why– it only makes sense to minimize your spending and maximize income if your goal is to retire as early as possible. If you’re that type, this book is for you.

But what if you’re the budding mini-philanthropist type who wants to leave a legacy by helping as many people as possible?? There are many instances that I can think of where more is actually better. If I have more, I could build a school or a hospital back home and help the lives of thousands of people, for example.

Overall, there is no denying that this is a great book with a different perspective on money and how to handle it. Of course, wasting your life on things that won’t make you happy is not the same as getting flat-out killed by a thug who wants your money– I was exaggerating to prove a point.

But just the same, keep in mind that our life here on earth is extremely limited. We cannot afford to buy progressively luxurious kinds of stuff that will suck a tremendous amount of our life energy (think about the SUV that you needlessly bought new!), especially if they don’t contribute to our well-being and happiness.

Or we would end up working for someone else our entire lives. Like a hamster on a spinning wheel, our lives would be miserable and pointless.